Contrast View

Contrast View

Increase Text

Increase Text

Decrease Text

Decrease Text

Reset Text

Reset Text

PMI signals a lull in June, but growth outlook strengthens

Future business expectations strengthen in June

Firms' margins and delivery times improve

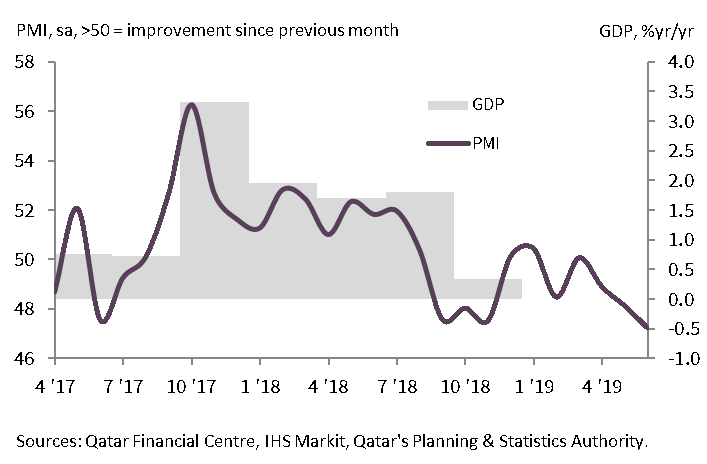

PMI consistent with tepid growth in second quarter of 2019

The most recent PMI™ survey of Qatar pointed to a stronger 12-month outlook for business activity, which was held back somewhat by a collection of local factors and aggravated by observed seasonal trends.

The Qatar PMI indices are compiled from survey responses from a panel of around 400 private sector companies. The panel covers the manufacturing, construction, wholesale, retail and services sectors, and reflects the structure of the non-energy economy according to official data.

The headline figure is the Purchasing Managers' Index™ (PMI). The PMI is a weighted average of five indices for new orders, output, employment, suppliers' delivery times and stocks of purchases, and is designed to provide a timely single-figure snapshot of the health of the economy every month.

The PMI eased to 47.2 in June, and averaged 48.1 over the second quarter. The quarterly PMI figure can be compared with changes in official gross domestic product (GDP). Since the survey began in April 2017 the PMI has a correlation of 0.88 with the year-on-year percentage change in GDP in real terms, over a comparison period of seven quarters up to the fourth quarter of 2018. The PMI is released ahead of GDP data, and accurately signaled the slower official growth rate of 0.3% year-on-year in Q4 2018. So far in 2019, the PMI is signaling a pick-up in GDP growth in the first quarter, to around 0.9%, followed by no change in the second quarter.

The easing of the PMI in June reflected softer contributions from four of its five components, most notably output and new business. The sole positive contribution came from suppliers' delivery times (although this index fell in June, it is subsequently inverted for the PMI calculation).

More positively, the outlook for total business activity strengthened in June as the Future Output Index rose to 80.0. Around 63% of survey respondents expect higher workloads at their units over the next 12 months, with confidence strongest in the real estate & business services and construction sectors.

June survey data signaled further downward pressure on private sector input costs. Prices paid for raw materials fell the most since the series began in April 2017. Overall input costs fell for the second month running and at a slightly faster rate than in May, also reflecting a stronger decline in staff costs. In contrast to input prices, the index for output charges moved higher in June, suggesting a relative improvement in firms' margins. Charges continued to fall overall, but by the least since February 2018.

The pace of Qatar's non-energy private sector expansion has tempered at the midway point of 2019, however it is foreseen to pick up again after the traditionally slow summer season given strong future orders. This follows a rebound in growth in the first quarter according to the PMI, up from 0.3% in the final quarter of 2018.

Slower current growth in Qatar partly reflects global headwinds: the global PMI* has now eased for four successive quarters up to the first quarter of 2019, and a subdued trend has continued so far in the second quarter.

Looking ahead, the 12-month outlook for business activity strengthened significantly in June. Promisingly, there was also evidence of improving margins for non-energy private sector companies, with a fall in the input prices indicator contrasting with a rise in the output charges indexSheikha Alanoud bint Hamad Al-Thani, Executive Director, Business Development, QFC