Contrast View

Contrast View

Increase Text

Increase Text

Decrease Text

Decrease Text

Reset Text

Reset Text

Qatar's Economy in a Strong Rebound Surpassing Regional Peers

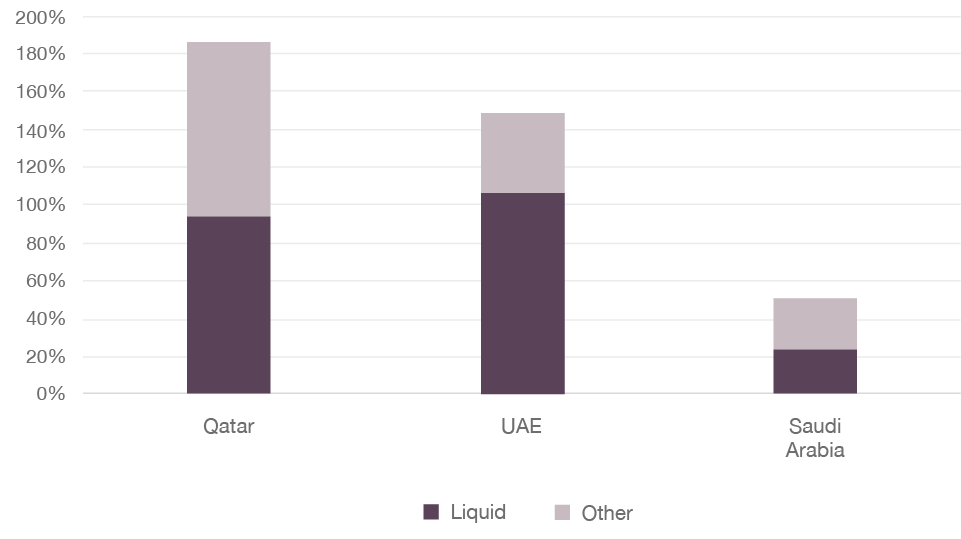

Qatar entered the COVID-19 pandemic on a stronger footing than its regional peers, with access to sizeable sovereign financial assets. These resources, along with effective fiscal policy adjustments during the year, ensured Qatar retained investment-grade ratings with all three major rating agencies, which have not fallen throughout 2020. On the back of this investor confidence, during the second quarter of the year when hydrocarbon prices faced severe pressures globally, Qatar issued a $10 bn Eurobond that was oversubscribed nearly 4.5 times.

Gulf Sovereign Financial Assets (% of GDP)

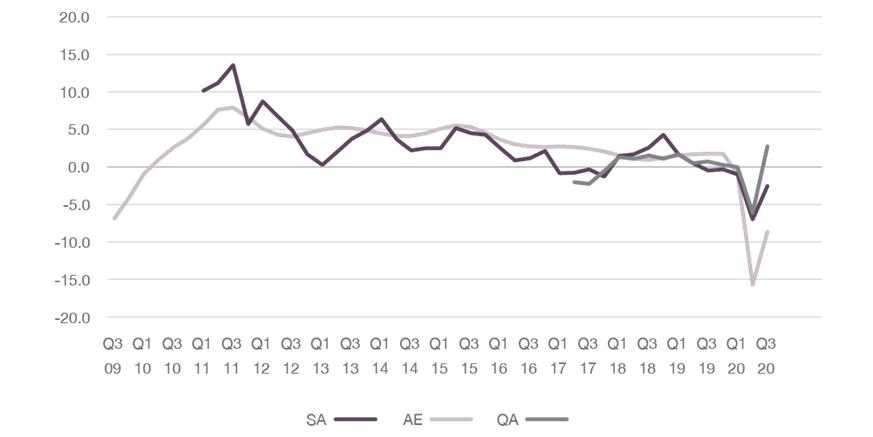

Despite challenges presented by COVID-19 to global economies in late 2020, within the Gulf region Qatar’s economy is outperforming its peers. Data on activity shows that after respective lockdowns activity throughout the Gulf’s major economies has returned – but the resurgence has been uneven. Qatar is currently experiencing an unparalleled recovery, judging by IHS Markit’s Purchasing Managers Indices (PMI), which signals the economy is expanding by a healthy measure over the past four months. Qatar’s strong headline PMI performance has been driven by a flood of new business orders and higher output, followed by increased purchasing activity of businesses and recovery of hiring trends. The robust recovery in Qatar is even more striking when considering that Qatar’s PMI average had been surpassed by a nearly 11% margin by its regional peers since the survey began in the second quarter of 2017. Supporting Qatar’s strong non-energy private sector performance is a wide-ranging government stimulus package, universal lifting of COVID-19 restrictions, and optimism surrounding future business.

Middle East PMI

The PMI tracks broad non-energy private sector performance, which is does through a regular monthly survey that covers multiple sectors and mostly mirrors national accounts data that are released with a delay. The PMI is one of the sole available leading economic indicators in the Gulf region, results of which currently suggest Qatar’s economy is leading the pack. PMI data generally has a high measured correlation with Gross Domestic Product (GDP), which stands at 0.65 (out of 1) in the State of Qatar. Whereas the correlation is weaker in the Gulf than other regions given the high weightage of both the energy and governmental sectors, which are not covered by the PMI survey, it continues to be a relatively accurate barometer of economic conditions. While the Gulf’s respective economies continue to be led by hydrocarbons production and government expenditure, long-term trends show a slow a steady movement toward economic diversification. Extrapolating from the observed headline PMI figures, national account estimates for both the UAE and Saudi Arabia continue to indicate contraction in the third quarter of 2020 while an expansion in Qatar is signposted.

Middle East GDP, %YY

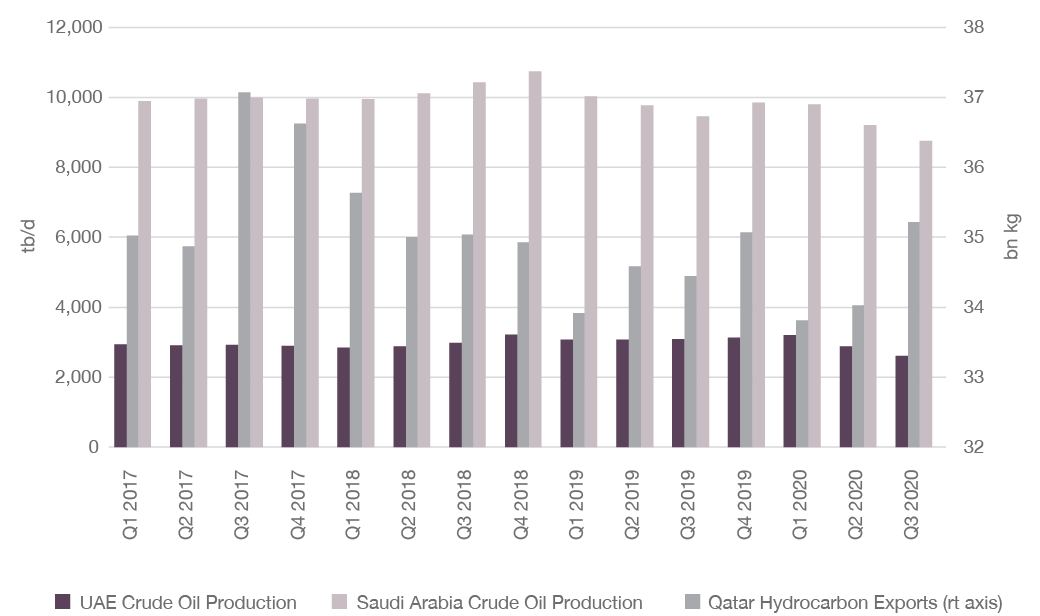

Economic performance disparity in 2020 may be wider still when considering activity of the hydrocarbon sector, which has been affected by OPEC+ cuts within Qatar’s peers. Whereas Saudi Arabia and the UAE are heavily dependent on crude oil production, Qatar has a more diversified hydrocarbon product suite that has been in higher demand during the COVID-19 pandemic. While energy demand has been subdued across the board over the past 9 months, crude & refined oil demand has been hard-hit given sharply lower global transportation needs. Resulting shrunken consumption of crude oil and its derivatives have driven OPEC+ to issue production curtailments. Both Saudi Arabia and the UAE have led the charge over the past quarters, with both countries posting crude oil production rates averaging nearly 10% less than the previous two years. Meanwhile, Qatar’s production and export of condensates, crude oil and natural gas is only 1.3% lower during the same period. Not only is Qatar no longer part of OPEC as of late 2018, it also benefits from the being the largest LNG exporter that continues to be used across major economies for electricity generation. While lower hydrocarbon prices affect the region as a whole, the lower observed production of hydrocarbons in Saudi Arabia and the UAE will undoubtedly translate into a slump in their national accounts’ figures.

Gulf Hydrocarbon Comparison

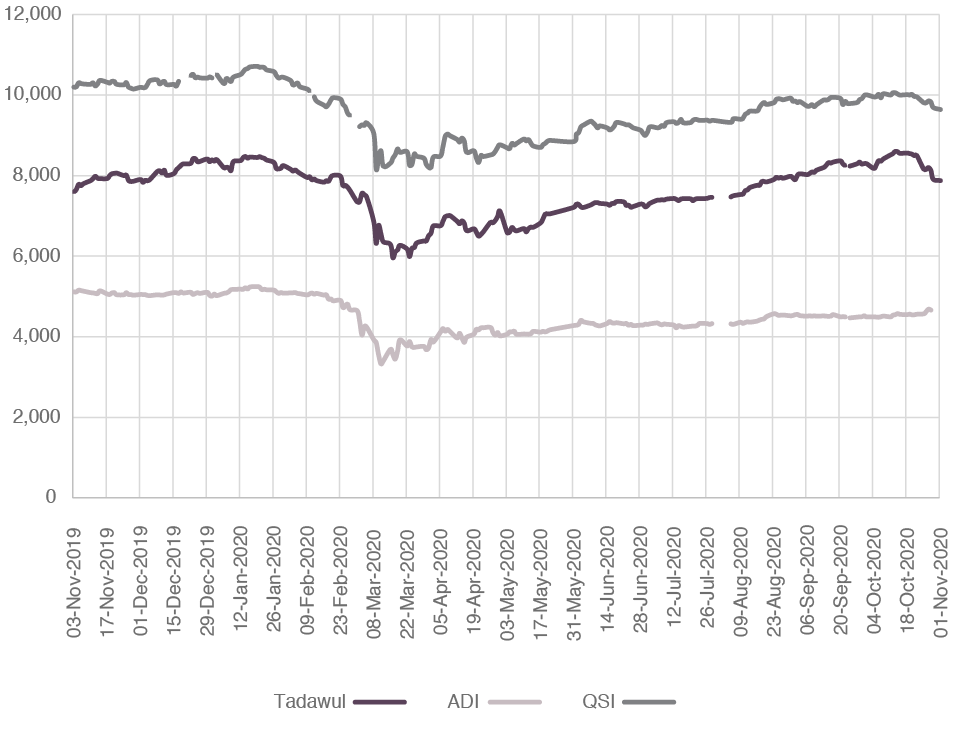

Financial markets have yet to factor in this economic disparity, with major Gulf stock market indices roughly in line with each other. This gap persists despite an increase in trading activity with Qatar ahead in terms of volume of trades during October 2020 standing at 2.96 times against those observed over December 2019, followed by Abu Dhabi (2.41 times) and Saudi Arabia (2.38 times). Performance year-to-date has been best in Saudi Arabia where the index’s close on November 1st is only 6.1% lower than at the end of 2019, followed by Qatar’s at 7.5% and Abu Dhabi’s at 8.7%. A variety of factors have contributed to this, including the launch of seven IPOs in Saudi Arabia this year and their commencement of derivates trading on August 30th. Meanwhile in Qatar’s stock market, preparations are underway for an IPO from a strongly-capitalized local firm and plans are afoot to connect to equity markets in China and Singapore to drive more activity. Once obstacles related to the current pandemic are tackled, visibility and activity are expected to increase leading to higher international investor interest in Qatar’s financial market.

Gulf Stock Indices

Looking forward, Qatar is poised for stronger economic expansion as compared to its neighbors given its FIFA World Cup Qatar 2022™ games, ongoing North Field expansion project, and the advent of two large free zones. Qatar has been preparing a wide variety of infrastructure and services in anticipation of receiving an estimated 1.5 million visitors for the FIFA World Cup Qatar 2022™ games. Simultaneously, its liquified natural gas capacity is set to expand from the current 14-train 77 mn t/yr operation to a 20-train 126 mn t/yr footprint between 2025 and 2028 according to latest industry estimates, which will also enlarge the volume of condensates and other by-products available for processing and export. The country has congruently been erecting two major free zones adjacent to its major airport and seaport that are already signing tenancy agreements with logistical, warehousing and light industrial firms. Together, these initiatives are set to not only see foreign direct investment rise but also promise significant economic expansion in the decade ahead.

Sources

-

- Moody’s Investor Service, Moody’s estimates, dated as of October 2020

-

- IHS Markit

-

- Saudi Arabian General Authority for Statistics (GaStat), Qatar’s Planning and Statistics Authority and Oxford Economics (quarterly

estimates for UAE) -

- IHS Markit provides the estimate for Q32020 GDP based on their PMI readings

-

- Succession of OPEC Monthly Oil Market Reports Table 5-9 and Qatar’s Planning & Statistics Authority (Foreign Trade Database

-

- Thomson Reuters EIKON pulled on November 1, 2020